Anatomy Of A Turnaround

We accidentally bought a turnaround. Now, to be clear most of the products we've purchased would fall into the distressed category. 2 have been proper distressed venture deals (former YC companies). But even the tiny ones that are half baked, I'd still consider those distressed. They are! You take them over, and you'll feel distressed!

Seriously though I want to talk through a deal that (to date) has not been a big win for us. What does that mean?

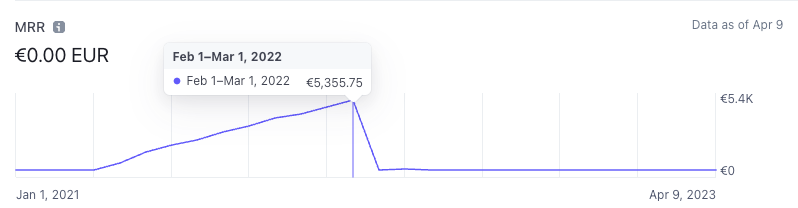

Some numbers first. This is the chart we were looking at when we bought it in March 2022. Looks great right? Up and to the right. Turns out there were a ton of annual subscriptions coming up for renewal ... and they didn't renew. We payed full price for customers we never got any $ from.

Notice these numbers are in Euros, which at the time meant ~$6k MRR. The steep drop is just us transitioning Stripe accounts because Stripe still hasn't figured out a way to transfer international accounts.

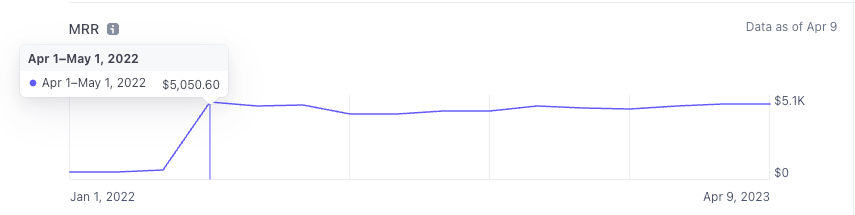

And this is what it looks like now. It's stable, flat. Slightly negative. Churn has stabilized, and so has the product. But still, not the growth we're accustomed to.

Cash collections after 1 year are about 40% of the purchase price. Relative to the performance of the rest of the portfolio, that's not a win. So what went wrong?

Diligence:

This one is tough. perhaps we could have talked to a few more customers, but boy is it difficult to get the time and the space in a competitive deal to talk to more than a handful of customers. It's also painful to set up, schedule, and dance around the topic of us buying the company. We usually go in to these conversations as "investors" doing diligence. It isn't typically a big deal but some founders get spooked by us wanting to talk to customers, so it's a bit of a dance.

I don't think there was something we "missed" in diligence that would have predicted the outcome.

Deal Structure:

I think this is where we missed. Two things happened:

- We made the seller financed payments based off of Chart Mogul reported MRR which was (and still is) wildly inaccurate. Up to 20% off from reality. We no longer use Chart Mogul because of how inaccurate it is. Because of this, our seller financed payments were tied to this inflated number and we over payed on the seller payments. The sellers got nearly their full earn out. Our mistake, a contract is a contract.

- Annual payments. Annual payments should be discounted for early stage companies. There's not enough history to reliably say what the renewal rate is on annual subscriptions. We will now, until the end of time (so long as we can get a seller to agree to it) prorate / discount annual payments. We absolutely don't mind paying up if they renew but this is a new area of downside protection we had previously ignored. It could have been partially due to this being the largest deal to date and larger deals have more annual subscriptions to factor in.

Turning The Corner

We're not out of the woods yet, but we did decide to invest in a significant front end rewrite. The product looks much more modern and fresh. That plus the added stability of the system should mean higher retention. We also did a bold thing (something I've found difficult to do when building from scratch) and removed features. When you're just starting out with a product, you will likely say yes to reasonable customer feature requests. a year or two of that though and you end up with a Frankenstein product that's complicated and difficult to use. I'm going through this now with Super Send. It's a little easier as an acquirer to have some distance to look and say "nobody is using these features, let's just kill them".

We hired a dev shop to do some designs for us to help us think through the rewrite. We spent about $2k-$3k and then ended up just buying and using a template for $100. lol.

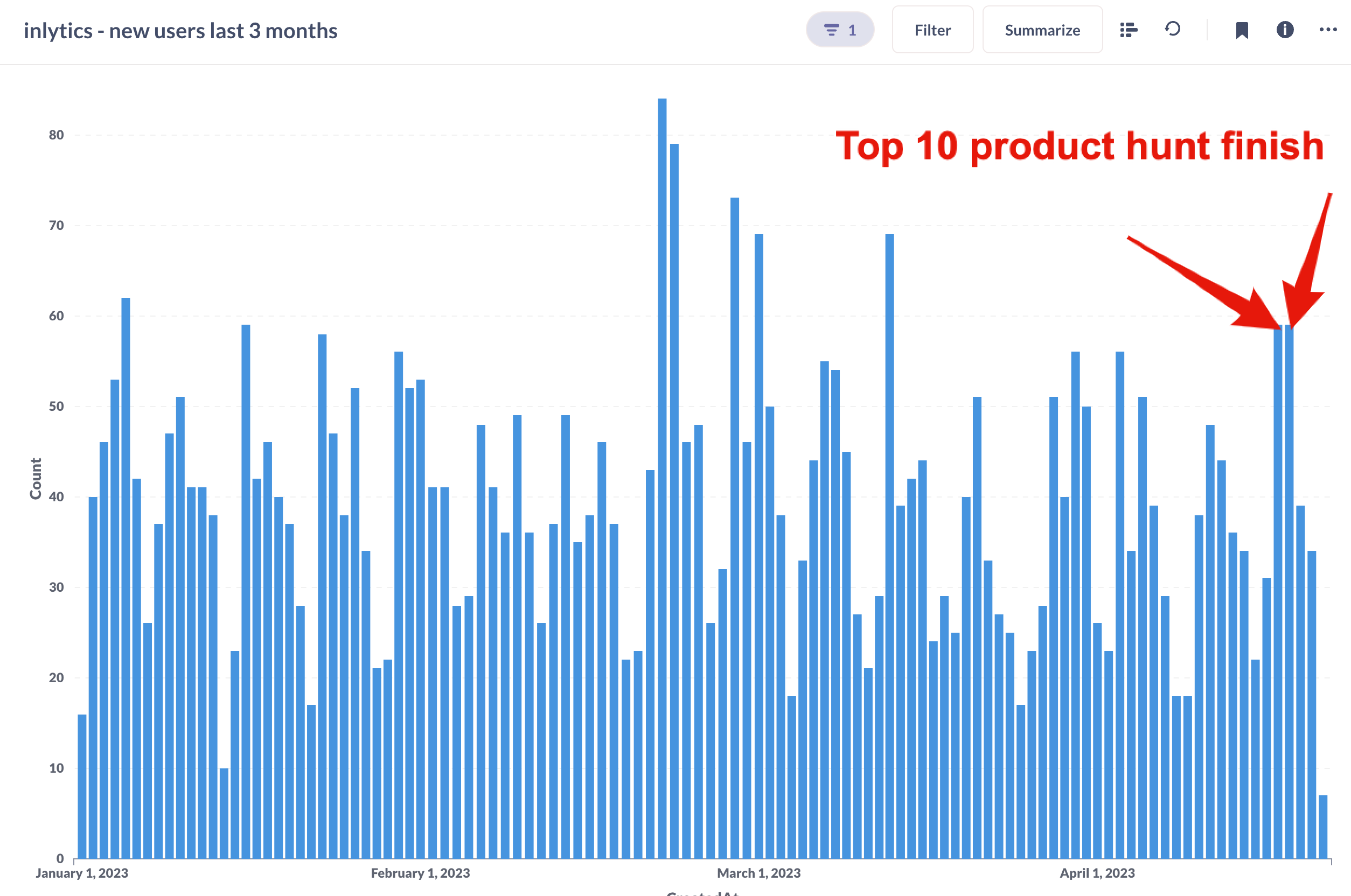

The rewrite took 1 dev 3 months. We then planned a re-launch on product hunt.

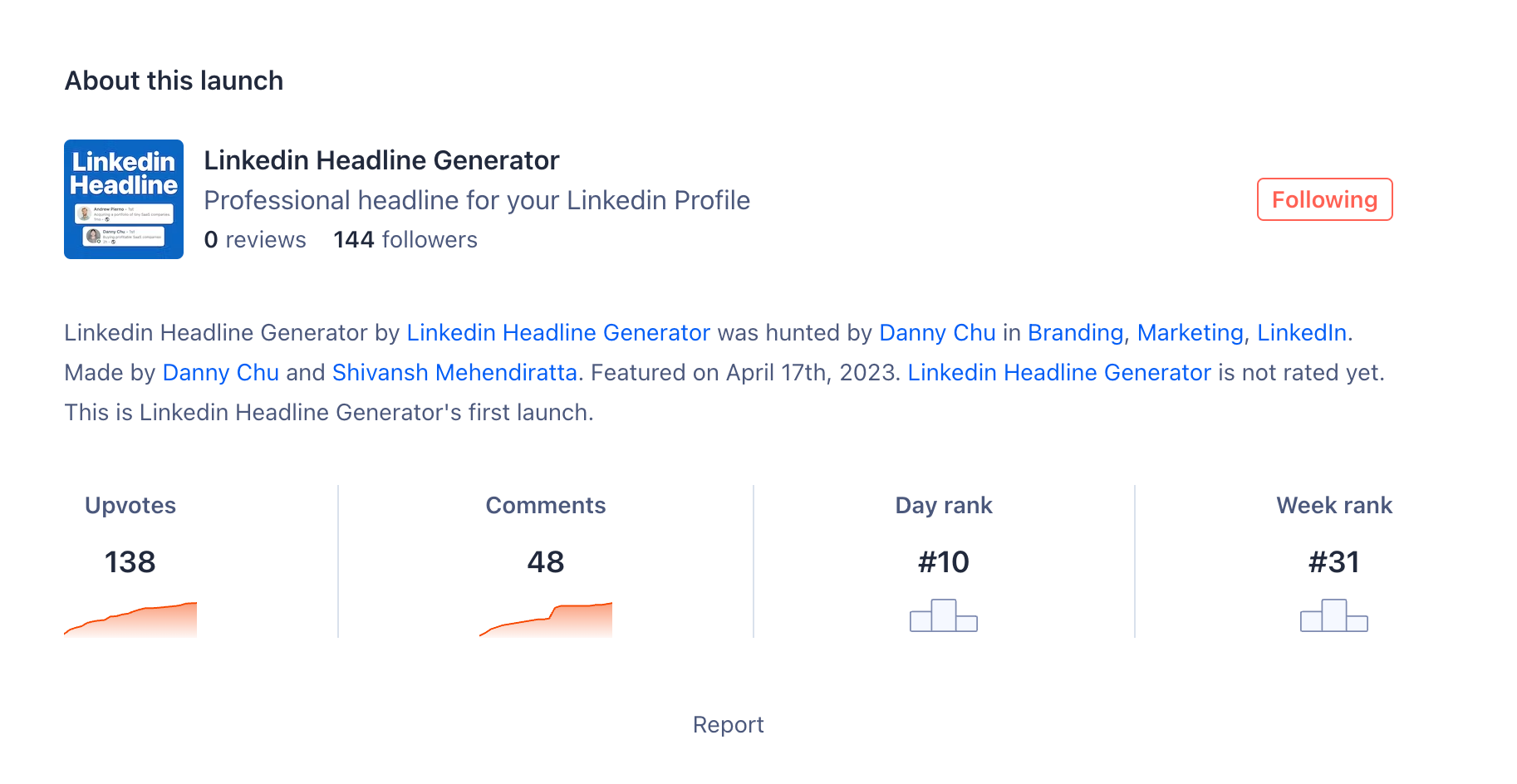

We didn't actually (yet) relaunch the v2 on product hunt. We did however release a growth tool to try and drive traffic and nearly cracked the top 10 for the day. Even this small amount of upvotes can really boost top of funnel and drive sales. The problem with growth tools is of course they require a very expensive resource (engineers) to create.

The Product Hunt launch went really well. We landed in the top 10 for the day and had a mild increase signups for a few days. The Product Hunt of today is not the same as it was a few years ago, it's not the magic bullet it used to be and is also an interesting data point on building tools as marketing (engineering as marketing).

It's still too early to say what kind of outcome the rewrite will have. We're aiming primarily to lower churn and hope the simplified rewrite more obviously delivers value to people. Obviously growth is nice, but customer acquisition hasn't historically been the problem, it's retention.

TLDR;

- Annual payments are a risk, and should be discounted or prorated. Bake it into the contract to have a variable payment based on the renewal rate of the annual customers. Otherwise you will pay full price for annual payments and never see a single dollar from these customers if they churn.