Fundraising Like A Roman God

We're raising capital for the first time to fund a new acquisition. This post is not a solicitation of investment, but a dialog about our fundraising process and experience.

Sorry for the clickbait. The title is aspirational. If you are able to fundraise like a Roman God, please write a book, give me the draft, and never publish it!

There are a few misconceptions about what we're doing here. Hopefully I can clarify with some of our intentions:

- We're trying to bootstrap the company to a place where we can dictate better terms and not get watered down in a fundraise. Fundraising for this company will be everything. XO Capital is basically a somewhat complicated math problem.

- We're going for venture scale returns with a private equity front door. We aim to buy on PE multiples and sell on strategic / venture multiples. The key is to understand we don't need venture scale returns to make the model work though, and that's a huge difference.

- It is my intention to one day take XO public.

Raising money is a slog. Oddly, it's one I happen to like. Nothing prompts a frank conversation quite like a pending wire transfer. You also often get to meet smart, thoughtful people.

The first week has been a little rough. To date, XO has put up 100% of the cash to buy our little portfolio of 4 companies. The three of us are in it around $100k each. A lot to some, not so much to others. It's a lot to us and it's obviously unsustainable given we're not sitting on a mountain of cash. Since we can't keep buying these things ourselves, we're going to need outside capital. And to raise some cash, we're going to have to find a simple way to explain our structure, make sure incentives are aligned, etc.

I've been told raising a fund is the hardest fundraise there is. LPs (the people who invest in funds) have to effectively just trust you to do the right thing with their money. That's not a difficult conversation if you have a track record of 20 years and some unicorns under your belt. It's different for us. We're not expert fund managers (yet!). We used our own cash to prove out the model and build a track record. Given the conversations I've had this week, I can see why they say raising for a fund is tough.

We've been looking for the right deal to bring to our small pool of potential investors. It took a lot longer than I thought it would. About 5 deals have fallen through since December that we thought might be a good fit. We have our very first deal we're trying to raise against. I won't talk about the deal specifics here (ping me if interested), but I do want to talk through how we're thinking about our model for these next few acquisitions.

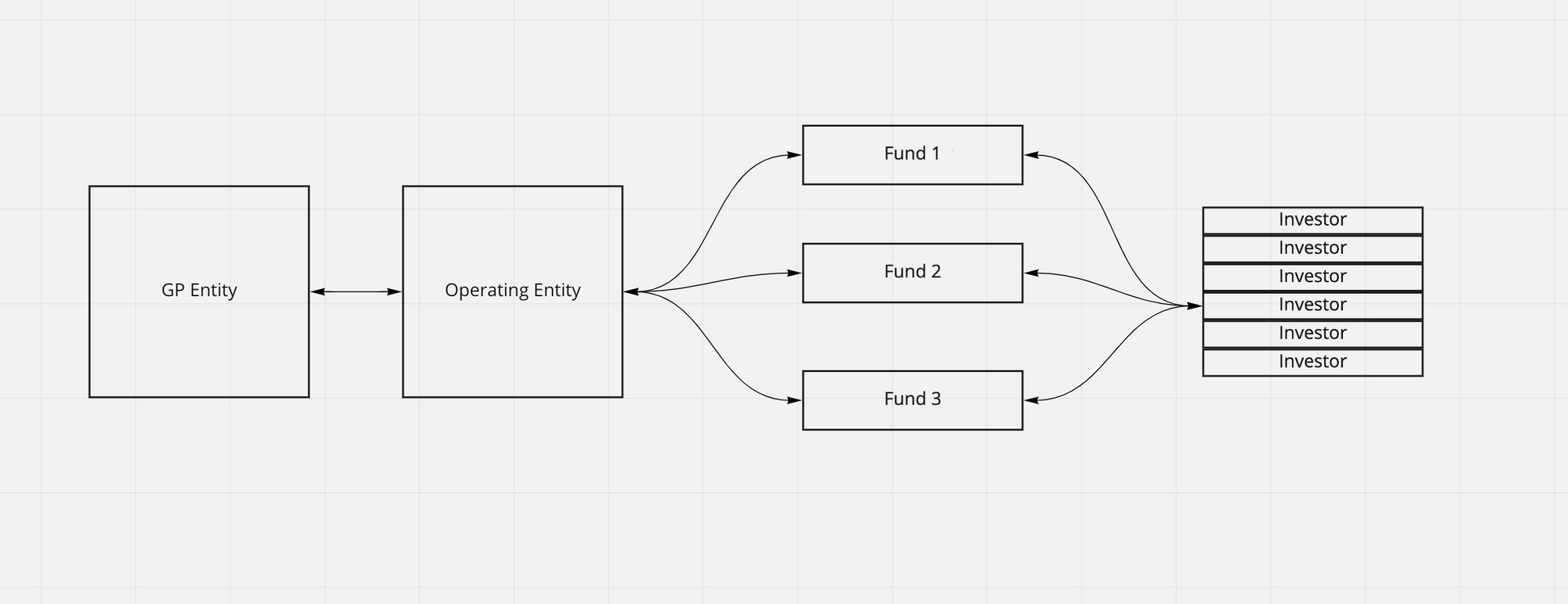

How a fund is normally structured.

Ever heard of 2 & 20? It's a traditional fund structure where you take 2% (annually!) of the fund to pay for expenses and get a 20% carry on the equity in the fund. This is the fund operator's (the GPs) incentive above the financial commitment they made into the fund. This works marvelously when you're just investing. It starts to get a little funky when the fund itself is operating the acquisition.

The above image is a mostly representative structure of a normal fund. It can get a lot more complicated than this but this should suffice. The GP entity has the partners (think founders). The business operational expenses (EAs / GP salaries etc) might come out of the Operating Entity. The equity is held in the GP entity for Funds 1, 2, 3. Investors get shares in each fund as LPs.

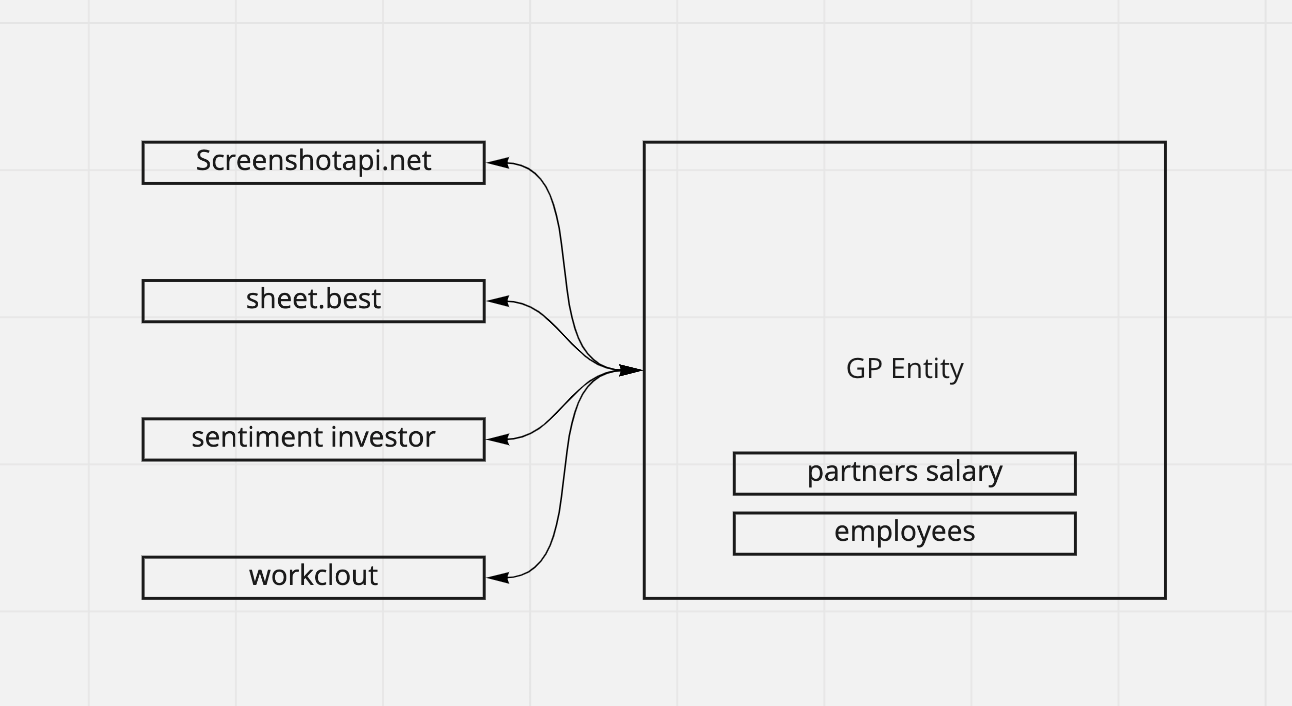

The works wonderfully most of the time. It works great for venture. It would even work great for us if not for a rather large caveat... we're also the ones who run the businesses after we buy them. Our structure is like this:

We're not fully set up as a proper fund. That's expensive to do. This is a single LLC with 3 people on the cap table. There are about 4 other LLCs we burned through before consolidating into one when Danny joined us.

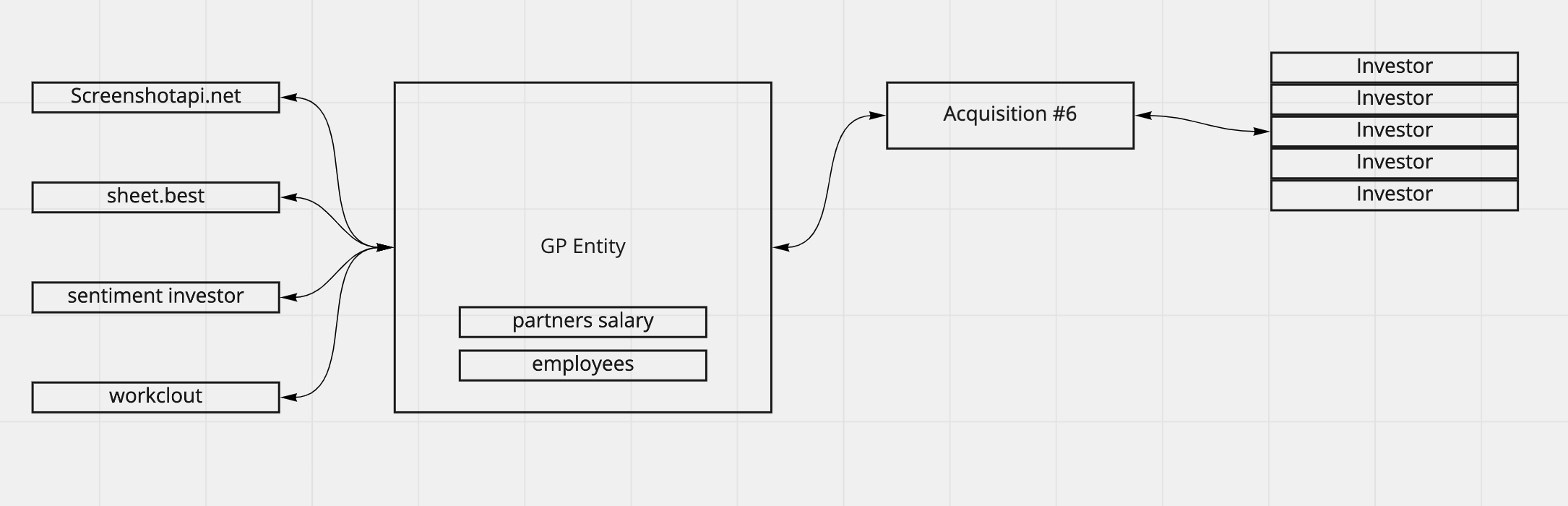

So here is where the problem lies. When we go out now to raise money for company #5 (acquisition #6), we're asking investors to effectively trust that we're going to operate it effectively along side our current portfolio.

I got a variation of this question a lot: "Andrew how much time are you personally going to spend on my investment". It's a valid question. The simplest way to answer that is we will track time and bill against the portfolio company for time we spent on it. It's annoying for us, but at least investors know the accounting is correct. But that's not really the question. I think the question is more like "Andrew, how much of your mental headspace is my investment going to occupy in your brain". That's a harder question to answer.

See we're buying tiny SaaS businesses. They're not big enough to support a full independent team. Our intention is to grow them to eventually be able to support that, but the moment we buy them, they are not able to support anyone at all. Even at $20k MRR after costs, it's hard to employ even 1 US based software developer at market rates.

Our solution to this problem of being too small is to use a shared services model. We have developers at XO as well as contractors, etc that can do work on one or many portfolio companies. When we buy a new business, we don't immediately need to hire people, we have great people here that can help initially. This is another source of confusion for potential investors since we're going to be billing our resource against the portfolio company (at cost).

Two Potential Solutions

1. Stay the course

We're going to continue trying to fund this deal in this way. We have a short but impressive track record of operating multiple businesses at the same time. We're posting good MoM growth while keeping expenses low. In short, the argument is something like we're great operators, that's why you should invest with us in this model in this way.

The second experiment in this same vein is our upcoming wefunder campaign for Workclout. We bought Workclout with our own cash, and we'll spin it out into a separate LLC and sell shares in Workclout and continue operating it ourselves.

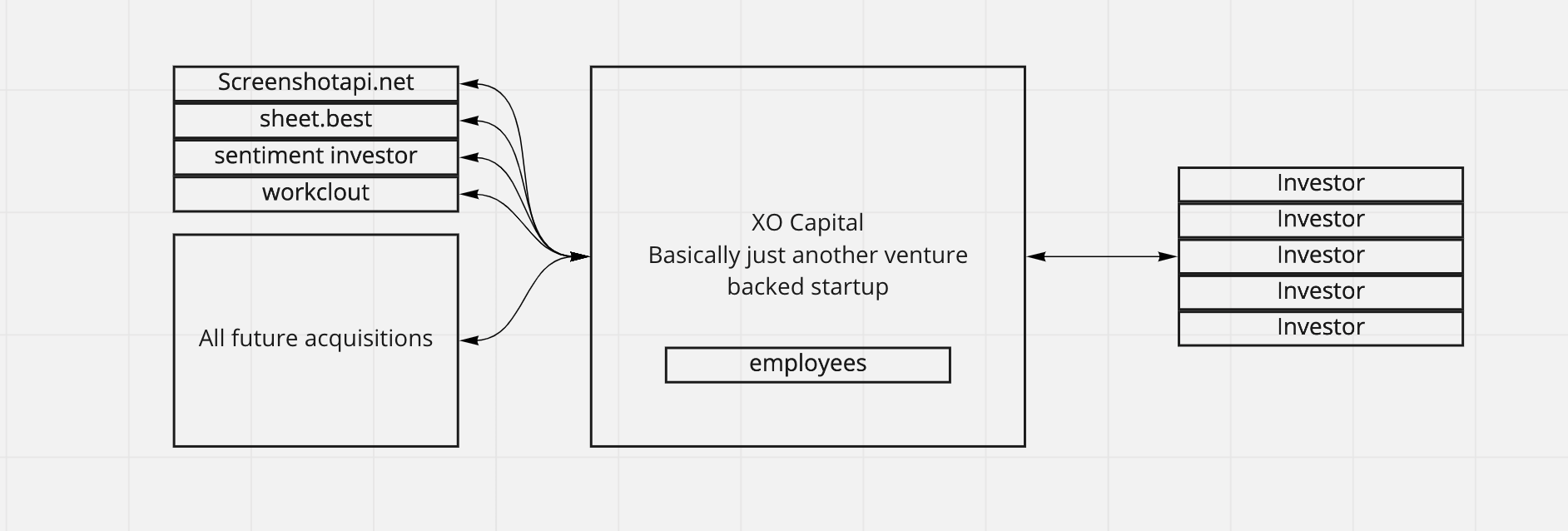

2. Consolidate into a single entity and sell shares of the GP entity so investors are buying exposure to our basket of companies.

This model is the most straightforward for everyone involved in terms of legal entities, etc. It looks like this:

This is a cool somewhat novel concept. Another example is look at Tyler Tringas' fund where he did a wefunder to get some cash in the GP. The reality is that small funds don't make any money. You only start making serious cash when you have a massive exit or you run multiple funds in parallel. preferably both.

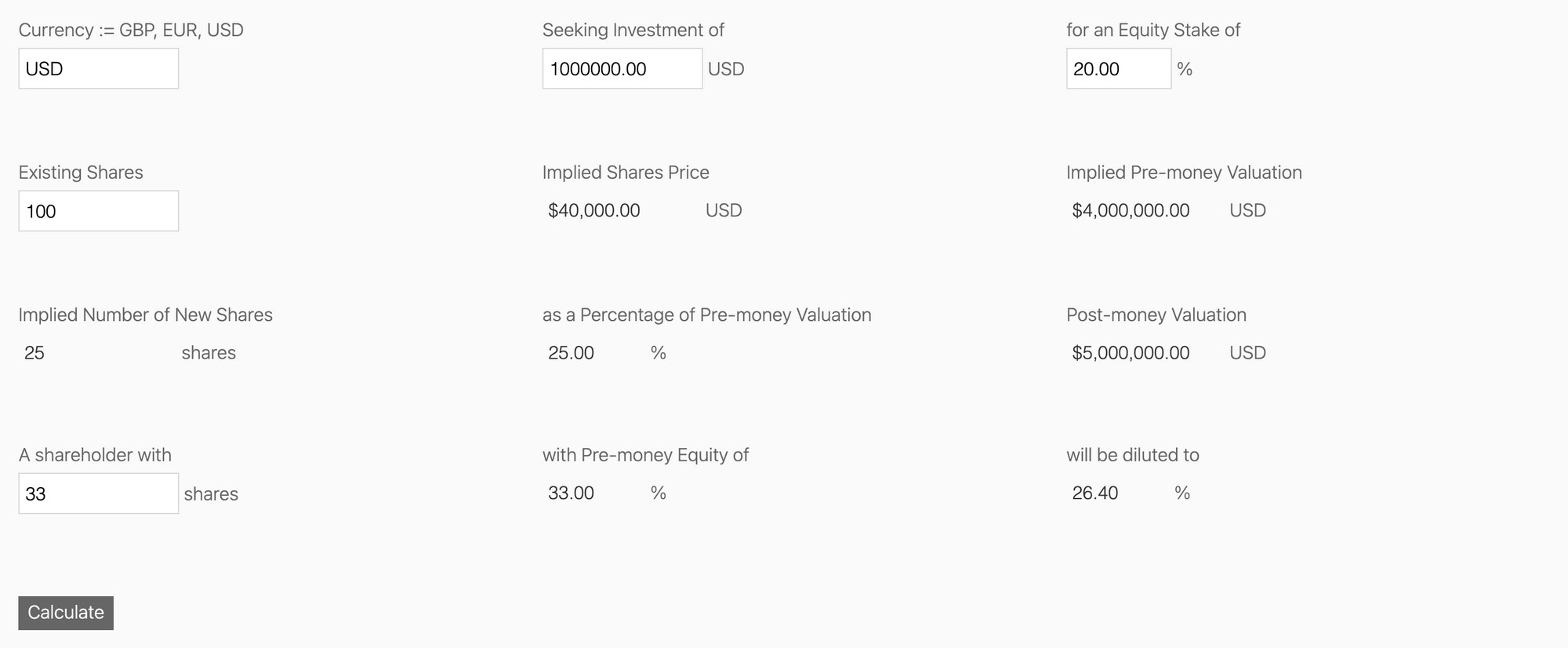

The problem with this model is that it kind of sucks for us as founders if we raise money too early. Nothing kills companies faster than a disincentivized founder. Here's a simplistic cap table scenario if we were to raise right now at a $4M pre and $5M post.

We're effectively taking a 7% dilution hit (each). (simple math / round numbers. we raise 20% of post money valuation at each round, dilution of 20% / 3 = 7%)

If we continue to raise money with roughly the same percentages then we'll take 7% dilution hits each time (again as 1 of 3 partners).

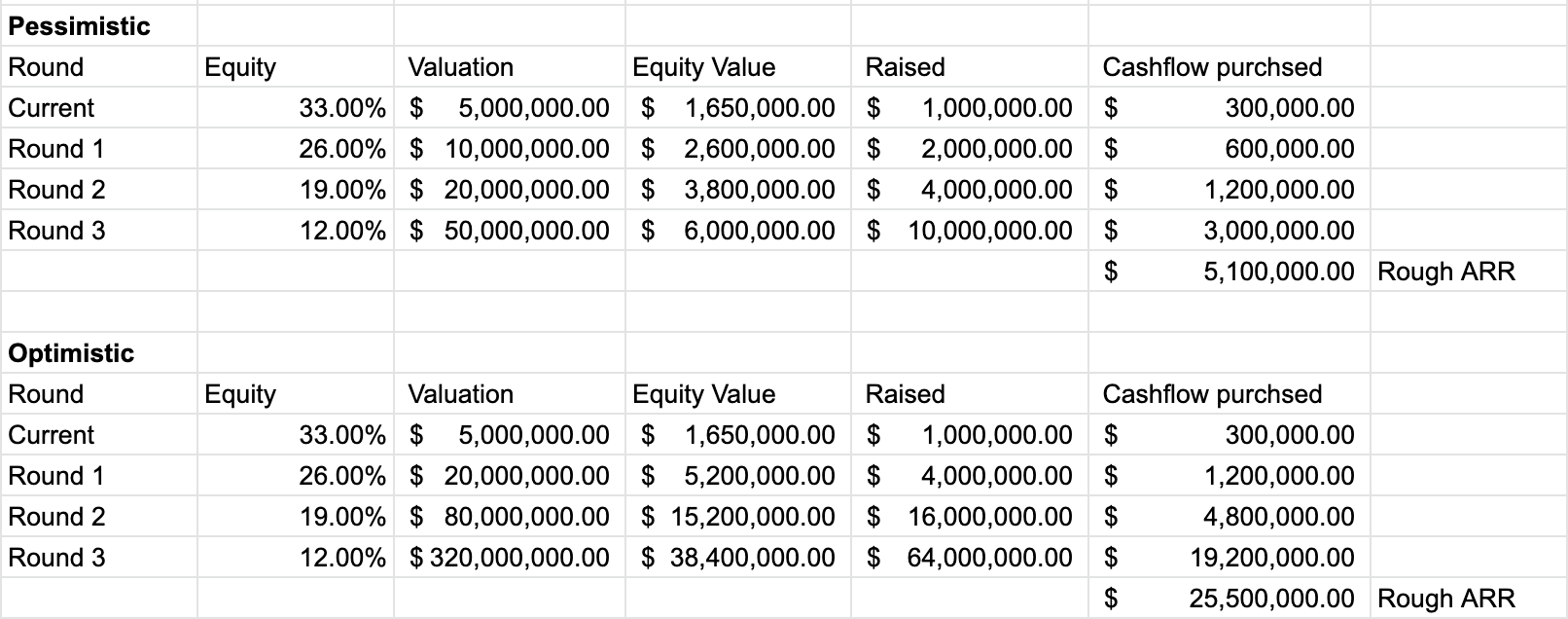

In a sense this chart is shows two pessimistic scenarios since there isn't any growth modeling in here. We assume we can continue to buy SaaS companies at a 3x-ish multiple.

Some might look at this and say this doesn't look bad at all. I mean who would complain about owning 12% of a $50M business? I don't know that I would! Depends how the relationship with investors is!

The point I'm trying to make is that the longer we can bootstrap, then the higher valuation we can fetch in that initial round, which has ripple effects all the way down.

Future (FAQ)

In summary, at the moment our belief is that at some point in the future we will consolidate all assets under one c-corp and run the company like a traditional venture backed startup. Investors participating in our one-off deals would eventually get shares in the GP. Probably going to be a good deal for these people since they helped us get off the ground.

What happens if one of these gets really big.

We're here to maximize growth, not necessarily cash flow. We'd either build a dedicated internal team with a dedicated internal CEO / GM and or we'd spin it out and raise venture to let it have a life of its own. If we do our jobs well, this will happen.

Have a great weekend.

✌️

Andrew Pierno